Crash Victims, Lawmakers To Hochul: ‘We Have A Better Idea To Reform Car Insurance’

ALBANY — Jermaine Lichtmore was driving his girlfriend to a Metro-North station in Westchester when a car driver ran a stop sign and hit his vehicle, tearing apart both shoulders and breaking multiple bones. He wasn’t able to return to work, and, eventually, his insurance coverage ran out, paying himself for surgeries and physical therapies while still dealing with ongoing pain.

Lynette Schinina, a physician’s assistant in Suffolk County, was rear-ended while stopped at a light — a crash that tore her rotator cuff. After multiple surgeries, she needed a full shoulder replacement and still has limited use of her right arm. She struggles to hold or lift objects, and has not been able to return to work. Her disability has run out and she lost her job and her home.

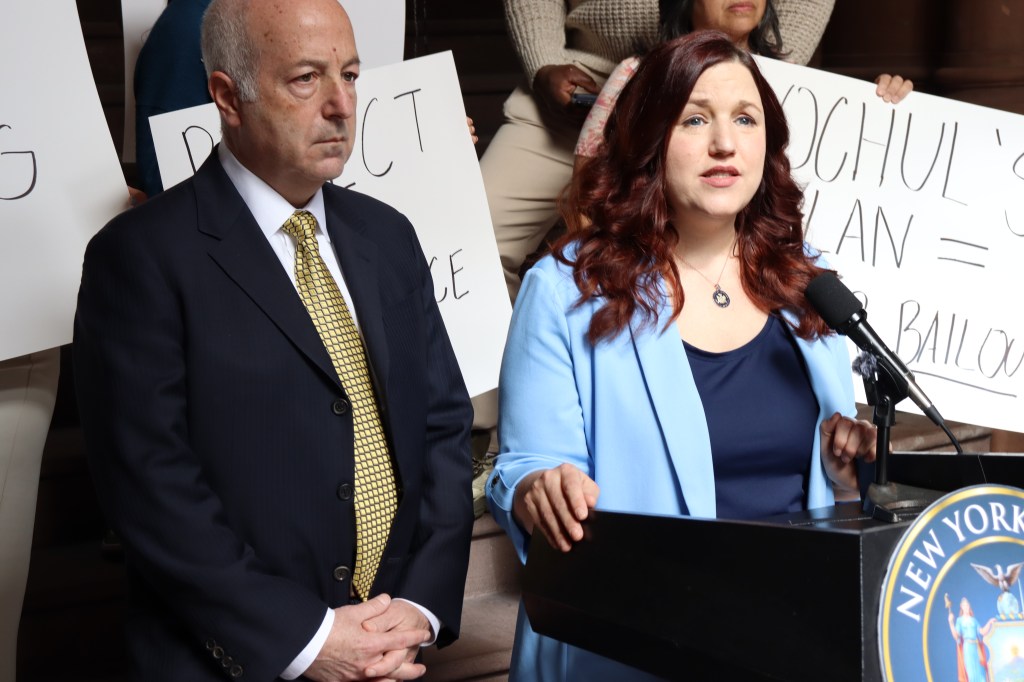

Both victims were at the state Capitol on Monday to decry Gov. Hochul’s proposal to reduce the cost of car insurance by making it harder for some victims to get full compensation for their injuries and to be made whole for crashes they didn’t cause.

“I wasn’t able to support my family, and it has been a very difficult road, especially having to be on medication every day and having to continue to go to therapy for pain,” Schinina said as she stood with Litchmore and other victims, plus victims advocates to oppose Hochul’s proposal.

“The lawmakers need to understand that this isn’t abstract,” added Litchmore. “This is real [people’s] lives.”

Lawmakers were also on hand to push legislative alternatives that, they say, will actually lower rates.

Legislation (A10524A/S9537A) from Assembly Member Jen Lunsford (D-East Rochester) and state Sen. April Baskin (D-Buffalo) would focus on lowering rates by changing the way insurers set the rates themselves.

The bill would prevent Big Insurance from setting rates based on a driver’s age, employment status, level of education, home ownership status or property value, credit score, past insurance polices, how likely said customer would find a new insurer if prices go up, ZIP codes (outside of auto crime and crash rates), or consumer data more than two years old.

The bill also allows the public to review rate increase applications from insurers, including their justifications, on the state Department of Financial Services’ website. Increases above 5 percent for personal car insurance and 10 percent for commercial car insurance would trigger public hearings. (The Hochul administration approved a 22-percent increase in car insurance rates in 2024.)

“I am an attorney, so I get lower rates for some reason. [And] if I have a higher level of education versus a lower level of education, I pay less than someone else,” Lunsford said. “Those have nothing to do with our actual driving records, with the likelihood of us filing a claim, things that have an actuarial basis in reality, for which someone might pay more. And I’m not saying people should all pay the same amount, but it gets at the root bias in so many actuarial calculations.”

Consumer Reports’ Chuck Bell told Streetsblog that ultimately, the Department of Financial Services needs to be more judicious when reviewing rate increase requests and identifying discounts for policyholders. Bell added that insurers have every reason to fear transparency.

“Companies have been really apprehensive because they don’t want people to know that they’re using [credit scores], and it would really freak them out if they knew that they were being marked up just because they missed a bill payment or something like that,” he said.

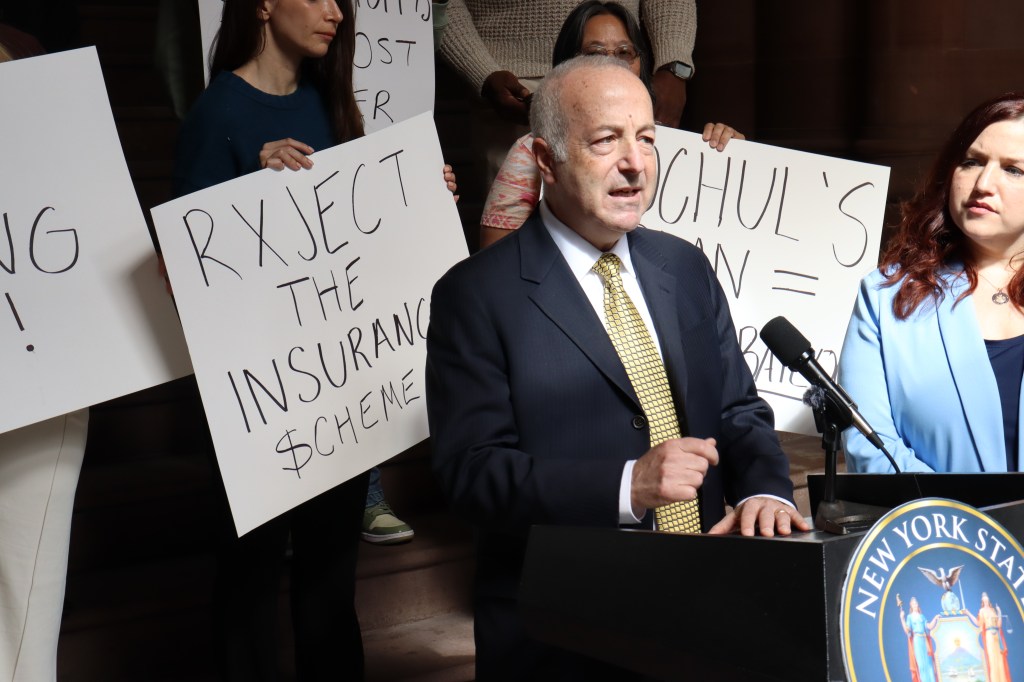

Tthe New York State Trial Lawyers Association staunchly opposes Hochul’s proposal because it would create a barrier to legal representation for victims. The group also resents being cast as “billboard lawyers,” “ambulance chasers” and “special interests” by the governor for two reasons: first, Hochul’s plan has the backing of $8 million in spending from Uber, whose CEO is also a Hochul donor. In addition, the MTA, which supports Hochul’s reform, has subways and buses that are literally covered with ads from those same “billboard” lawyers.

Andrew Finkelstein, the president of the lawyers group, said Uber’s support has robbed Hochul of objectivity.

“Frankly, she’s in the pocket of these insurance companies and Uber, and she’s carrying their water,” Finkelstein said.

The Hochul administration pushed back on that.

“You can’t make it up: one of Albany’s most powerful special interests is launching desperate attacks on Gov. Hochul for trying to save New Yorkers money and root out fraud, waste and abuse,” Hochul spokesperson Sean Butler said in a statement. “Right now, our broken car insurance system makes a few New Yorkers rich at the expense of skyrocketing costs for the many. It’s time we put an end to that broken system and get that money back in New Yorkers’ pockets.”

Lunsford and Baskin’s bill isn’t the only one being pitched by lawmakers to lower insurance costs. Assembly Member Jeffrey Dinowitz (D-Bronx) and state Sen. Jamaal Bailey (D-Bronx) introduced legislation that would force insurers to reveal the criteria used to set rates. Streetsblog has also reported that pay-per-mile and other insurance options could prove more affordable in New York than standard insurance.

Hochul’s car insurance proposal limits the ability of some crash victims to sue for damages related to pain and suffering by narrowing the definition of a “serious injury” as well as the types of victims eligible to sue.

The governor’s proposal hinges on the assertion that “jackpot” lawsuit payouts and fraud are driving up auto insurance rates, and that by creating savings for insurers, they will be able to pass on savings to policyholders once the state enforces long-dormant consumer protection laws.

But lawmakers, legal professionals, crash victims and members of the press have yet to find a connection between narrowing legal rights from crash victims and lower car insurance prices, turning what could have been a quiet election year budget into a protracted debate over affordability.

And for all her talk of “fraud,” the governor has yet to prove that much exists. And even she has claimed her reform would only save the average driver $25 a month on premiums.

The state budget will be late this year, and car insurance is one of a handful of policies demanding longer negotiation. So long as questions remain about tangible savings for policyholders, debate will drag on.

Read More:

Streetsblog has migrated to a new comment system. New commenters can register directly in the comments section of any article. Returning commenters: your previous comments and display name have been preserved, but you'll need to reclaim your account by clicking "Forgot your password?" on the sign-in form, entering your email, and following the verification link to set a new password — this is required because passwords could not be carried over during the migration. For questions, contact tips@streetsblog.org.